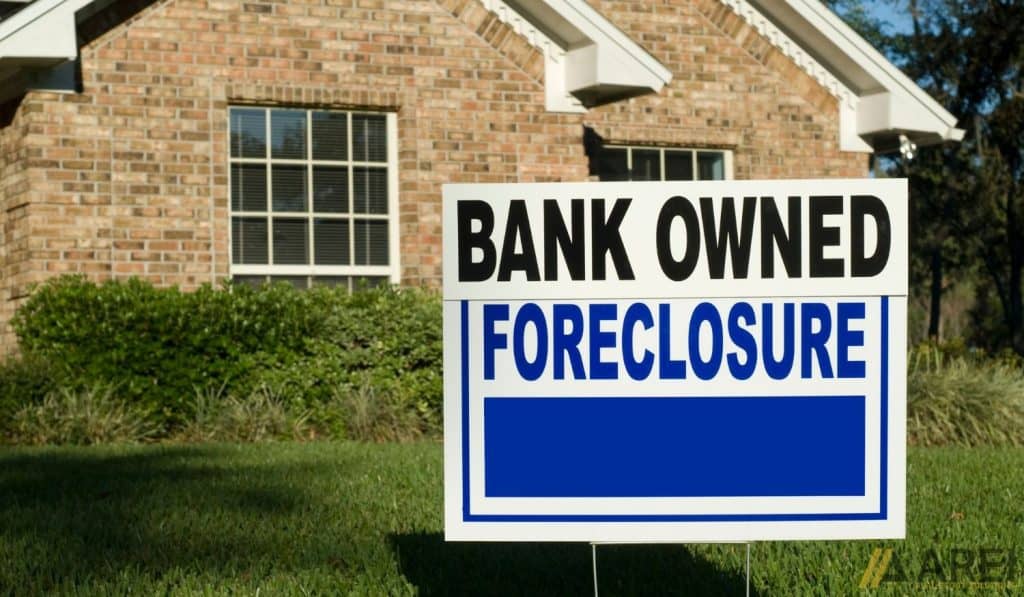

The numbers are clear. Foreclosure filings nationwide climbed 16% in the third quarter of 2025 from the year before. Bank repossessions? They shot up 33% right alongside. Here in Richmond, this trend creates complex situations for property owners and investors.

From our experience, navigating this requires a specific skill set. Effective distressed property management in Richmond, VA isn’t just about maintenance; it’s a strategic process to protect value and mitigate risk in today’s market.

This article provides owners and investors with actionable strategies. We’ll cover everything from understanding the local landscape to executing a recovery plan.

For a complete guide, explore our post on how to sell a distressed property. If you’re starting your search, learn how to find distressed property. Once you own one, our next post will detail how to sell distressed property successfully.

Short Summary

- Distressed property management requires quick, informed decisions to stabilize distressed properties and protect long-term value.

- In today’s market, rising costs, legal exposure, and timing pressures create both challenges and investment opportunities.

- Coordinated management helps owners and investors reduce risk, maintain assets, and support recovery.

- Understanding local laws and market dynamics in Richmond is critically important for sustainable outcomes.

Understanding the Landscape of Distressed Properties in Richmond, VA

Let’s break down what “distressed” really means here. It’s not just a run-down house. In our current market, a property becomes a distressed asset when the owner can’t meet financial obligations, leading to events like foreclosure or short sales.

This distressed real estate represents a significant segment of Richmond’s transactions. Why do these troubled assets exist? Common causes include excessive mortgage pressure, estate complications, or a business downturn.

We see three primary categories of these distressed properties:

- Residential: This includes single-family homes where owners face financial hardship. The goal here is often to avoid foreclosure and preserve some value.

- Commercial: Distressed commercial real estate is a major factor now. Think vacant office spaces in older downtown buildings or struggling neighborhood retail centers. These present unique challenges.

- Specialized: Assets like nursing homes are a world of their own. They combine real estate woes with strict regulatory compliance, making them highly complex.

Who’s involved? Financial institutions and institutional lenders like Wells Fargo often hold the non-performing loan. To clear their books, they may engage in loan sales, bundling these mortgages for other investors.

This is how properties become bank owned or REO.

Here’s an important lesson for borrowers and investors alike: Market value for distressed assets can be highly volatile. A property might appraise for one amount, but its true “distress sale” price is a different game.

As one veteran appraiser told us, “The market value is a theory until a motivated seller meets a ready buyer.”

Key Challenges in Distressed Property Management

Managing a distressed property feels like a high-stakes chess game. You face simultaneous moves on financial, legal, and operational boards. The core challenges stem from this constant pressure. Let’s outline the major hurdles.

Financial Pressure and Mounting Costs

The clock is always ticking. Cash flow is usually negative, and holding costs like taxes, insurance, and maintenance drain resources fast. What about deferred repairs?

We once took over a bank-owned home where a minor leak, ignored for months, led to a $15,000 mold remediation bill. A financial risk like this requires immediate and careful evaluation.

Legal Labyrinths and Exposure

This is where the risk escalates. You must navigate local laws, foreclosure processes, and potential bankruptcy matters. One misstep can trigger litigation. For example, improper notice to a tenant under Virginia law can stall your recovery for months.

Servicing agreements with lenders can be incredibly restrictive, limiting what an owner or management team can actually do. The question isn’t if legal issues will pop up, but when.

Stakeholder Dynamics and Human Factors

The human element adds another layer. Tenants may be fearful or hostile. Out-of-state sellers or borrowers can be difficult to reach. An heir inheriting a problem property often feels lost, not just financially but emotionally.

Aligning all these parties toward a common goal is a huge test for any management team. You need the right resources and services just to get everyone to the table. So, how do you move from problem to solution? That demands a clear strategy.

Effective Strategies for Managing Distressed Properties

Turning a distressed property around requires a clear plan and decisive action. Success hinges on moving fast, collaborating with the right partners, and understanding Richmond’s specific rules. Let’s explore the key strategies that protect value and guide a property to recovery.

Move Fast with a Clear Assessment

The first rule is to act quickly. Time always costs money in these situations. A swift, professional assessment is your roadmap. You must identify the core financial problem. Is it a cash flow shortage, a looming balloon payment, or major deferred maintenance?

Understanding this dictates your strategy, whether it’s restructuring the loan with lenders or planning a sale.

This ability to evaluate and protect the asset is non-negotiable.

Collaborate with Your Financial and Operational Team

You can’t navigate this alone. A strong team is your greatest resource. This means working closely with special servicers if it’s a Commercial Mortgage-Backed Securities (CMBS) loan, negotiating servicing agreements, and bringing in expert property managers.

A good property manager can maintain tenant stability, which preserves income during a transaction. As one lender told us, “We prefer a performing loan to owning property any day.” Your goal is to assist all parties—borrowers, lenders, clients—to find a common path. A creative structuring of a deal, like a debt-for-equity swap, can turn opposition into partnership.

Execute a Richmond-Specific Plan

Finally, your strategy must be local. For owners and investors in Richmond, this means tailoring your investment and disposition approach. Investing in the right improvements can maximize appeal to our local market.

A critically important factor is following Virginia’s local laws. Updates to the Virginia Residential Landlord and Tenant Act (VRLTA) effective July 1, 2025, change how security deposits are handled and late fees are calculated.

Using an outdated lease could contribute to major legal risk. Managing a distressed asset here requires knowing these rules to protect your clients and project.

Current Trends and Legislative Updates in Distressed Property Management

The landscape for distressed assets is always shifting. In today’s market, smart management means understanding both national financial pressures and hyper-local legal changes. Here’s what’s shaping decisions in Richmond for 2025 and beyond.

Market-Wide Pressures and the Distressed Pipeline

A major trend is the wave of commercial loan maturities. Many properties financed with low-rate debt a few years ago now face refinancing at much higher rates. This creates a pipeline of potential distressed assets. However, not all sectors are equal.

While office and retail face challenges, the multifamily sector in Richmond has shown notable resilience, often presenting unique opportunities for investors.

For borrowers, this market pressure makes early communication with lenders about restructuring more vital than ever to avoid foreclosure .

Key Legislative Updates for Richmond Properties

On the legal front, updates to the Virginia Residential Landlord and Tenant Act (VRLTA) are critically important for management. Changes taking effect emphasize transparency and fairness. Key updates include:

- Stricter rules for security deposit accounting and timelines for return.

- Clearer guidelines on charging late fees and other tenant costs.

- Enhanced provisions for handling property access and maintenance requests.

For any owner or investor, compliance is a major factor in mitigating risk. Using an outdated lease agreement is a direct risk to your investment.

Furthermore, the VA Home Loan Program Reform Act highlights the state’s focus on housing stability, which can influence deal structuring and finance options for residential properties.

Staying current with these resources isn’t just about following the law. It’s about protecting your asset’s value and your relationship with tenants.

Final Thoughts

Successfully handling distressed properties in Richmond requires focus. The challenges are real, but so is the potential. When you approach these distressed properties with informed management, you turn complexity into controlled recovery.

Understanding all these factors is critically important. It lets you protect your investment and find value where others see only risk.

Ready to learn more about navigating this market? Explore further insights and expert guidance on our website. We have resources to help you move forward with confidence. Visit our homepage to continue building your knowledge.